Back in July, we discussed how education level, marital status, and family structure can all affect your net worth which in turn can affect your financial stability. To learn more about the role those factors play, check out part one.

Thank you for reading this post, don't forget to subscribe!

Below, we will explore the other factors affecting financial stability and net worth focused on by the U.S. Net Worth Statistics: homeownership status, region, race/ethnicity, and age.

But first, let’s go over some definitions that might be helpful.

Definitions

When looking at real estate property and its effect on wealth, the terms home equity and net home equity often come up. Your home’s equity is the home’s current market value minus any remaining debts on the home. Net equity is basically the same thing. The “net” aspect typically only comes into play when calculating assets. This is more important in calculating insurance for your home including the materials inside of your home or for businesses that maintain inventory which would add to the equity.

HomeOwnership Status

According to the The Wealth of Households published in 2017 by the U.S.Census Bureau, homeownership is one of the largest contributors to net worth. The median net worth of homeowners is $254,900. The median net worth of renters is $6,270.

| Median net worth | Average net worth | Percentage of population | |

| Owner | $254,900 | $1,099,070 | 64.9% |

| Renter (or other) | $6,270 | $95,560 | 35.1% |

This isn’t really a surprise. Most people who own a home have a higher net worth with higher earnings than those that rent. Keep in mind that the net worth is an accumulation of your assets minus your debt. Owning your own home, even when you are still making payments on it, adds to your assets which increases your net worth. Your home is not only an expense. It is adding to your net worth. A portion of your mortgage goes to paying the principal of the house. So with home ownership, you are taking the money and it is being added to your net worth. When you rent, the money does not factor into your net worth.

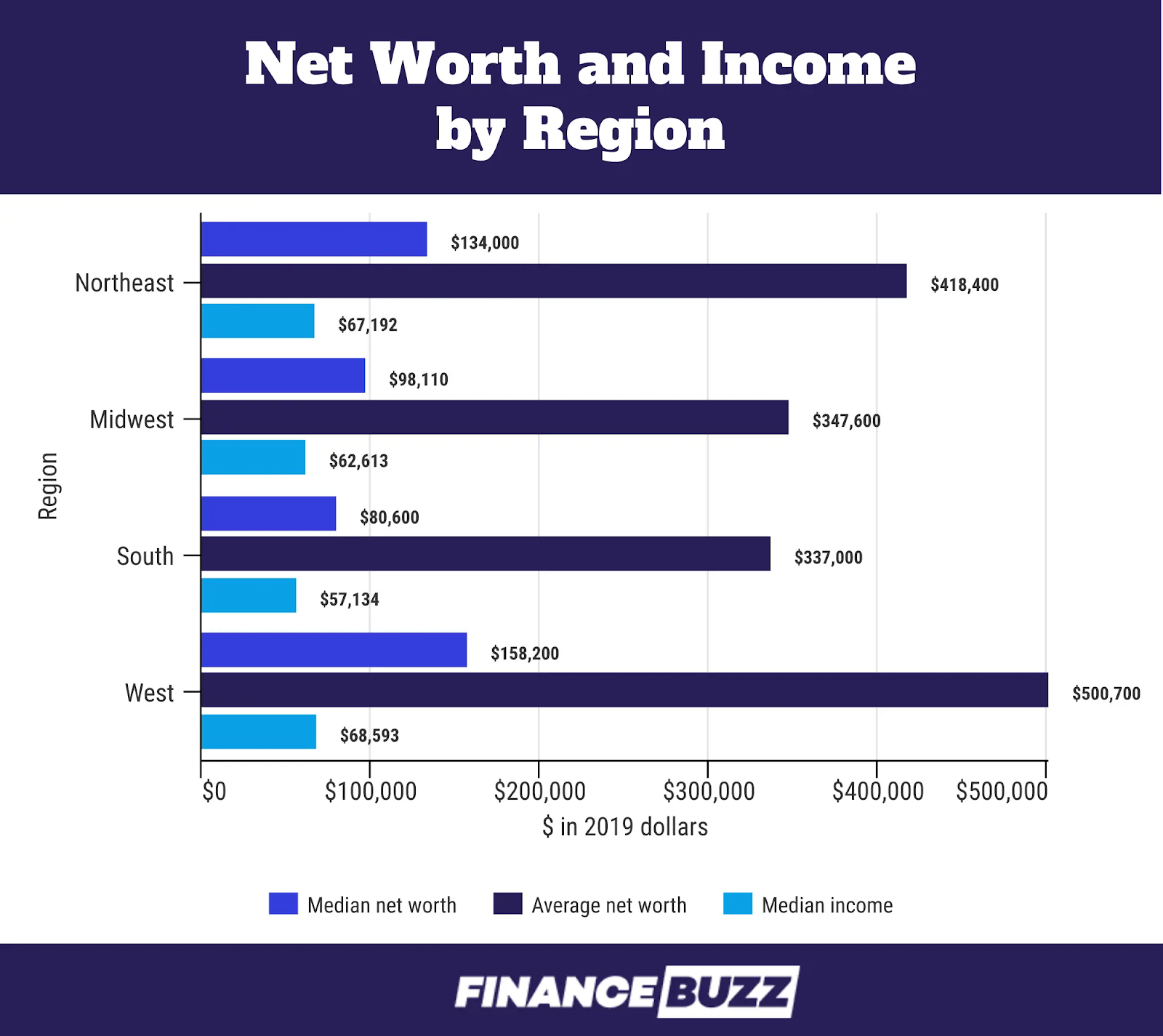

Region

Your region can also have an impact on your net worth. There are regions of the country that do not have as high of an access to as many resources to help with upward mobility. For example, the median net worth in the Northeast is $134,000, in the Midwest the median is $98,110, in the South it is $80,600, and the West has a median net worth of $158,200.

When you look at the median income in each region, the numbers become more interesting. You may expect there to be a similar gap between the incomes as with the net worths, but you would be wrong. The Northeast has a median income of $67,192 while the Midwest has a median income of $62,613. The income level plays a role, but the home equity in each region also has a discrepancy ($100,000 in the South vs. $200,000 in the West). The home equity being double plays a more significant role than the income. Not just your home equity, but the region in which your home equity is based, impacts your net worth.

Race/Ethnicity

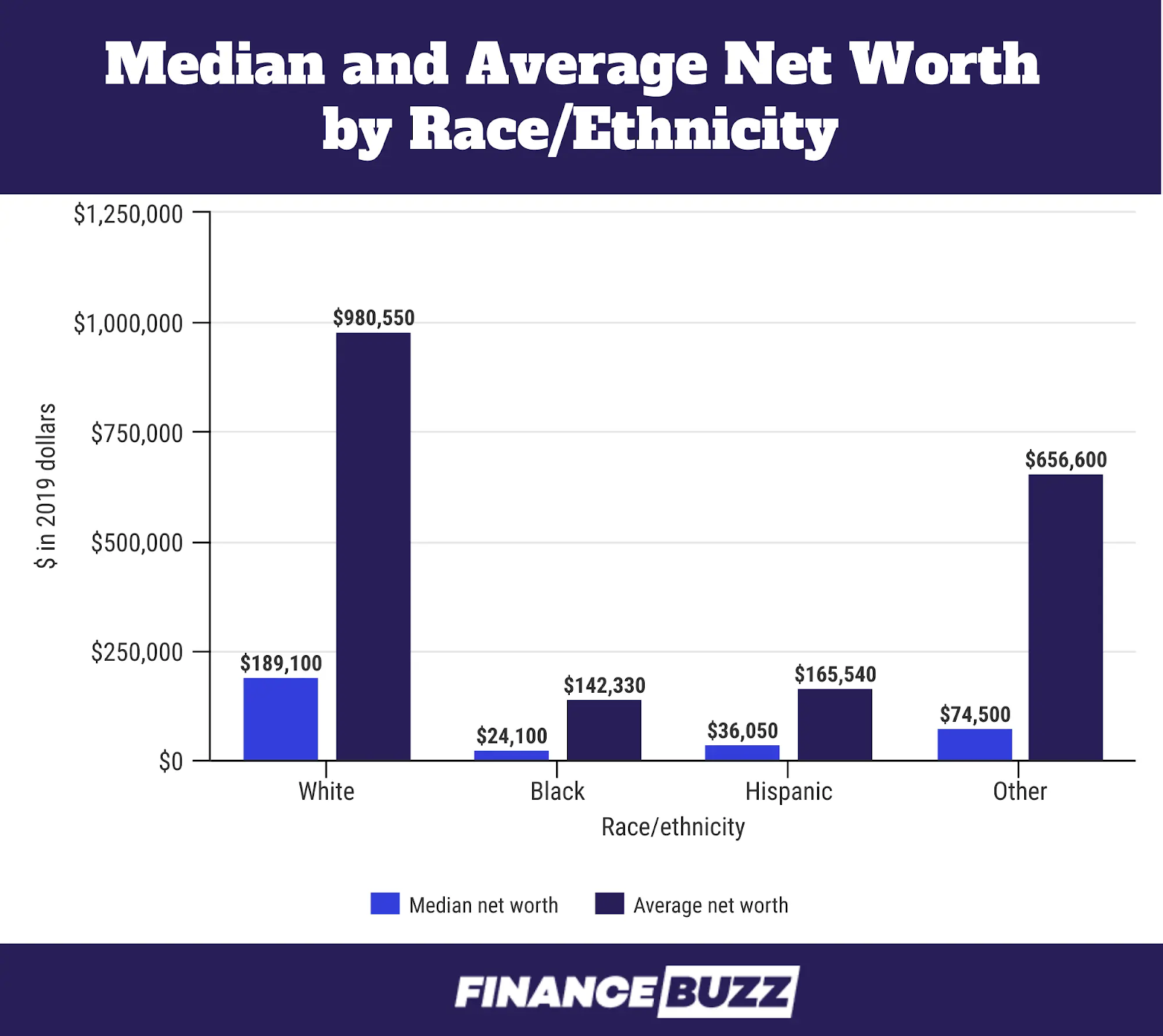

Race/ethnicity also plays a role in net worth. The median net worth for a white family in 2019 was $189,100 while the median net worth for a black family in 2019 was $24,100. The median net worth for a Hispanic family in 2019 was $36,050, and the median net worth for those families identified as a race/ethnicity other than white, black, or Hispanic was $74,500. This is a huge discrepancy. There are many factors that contribute to this discrepancy, but the fact remains that race/ethnicity is a significant factor that affects a person’s net worth.

Age

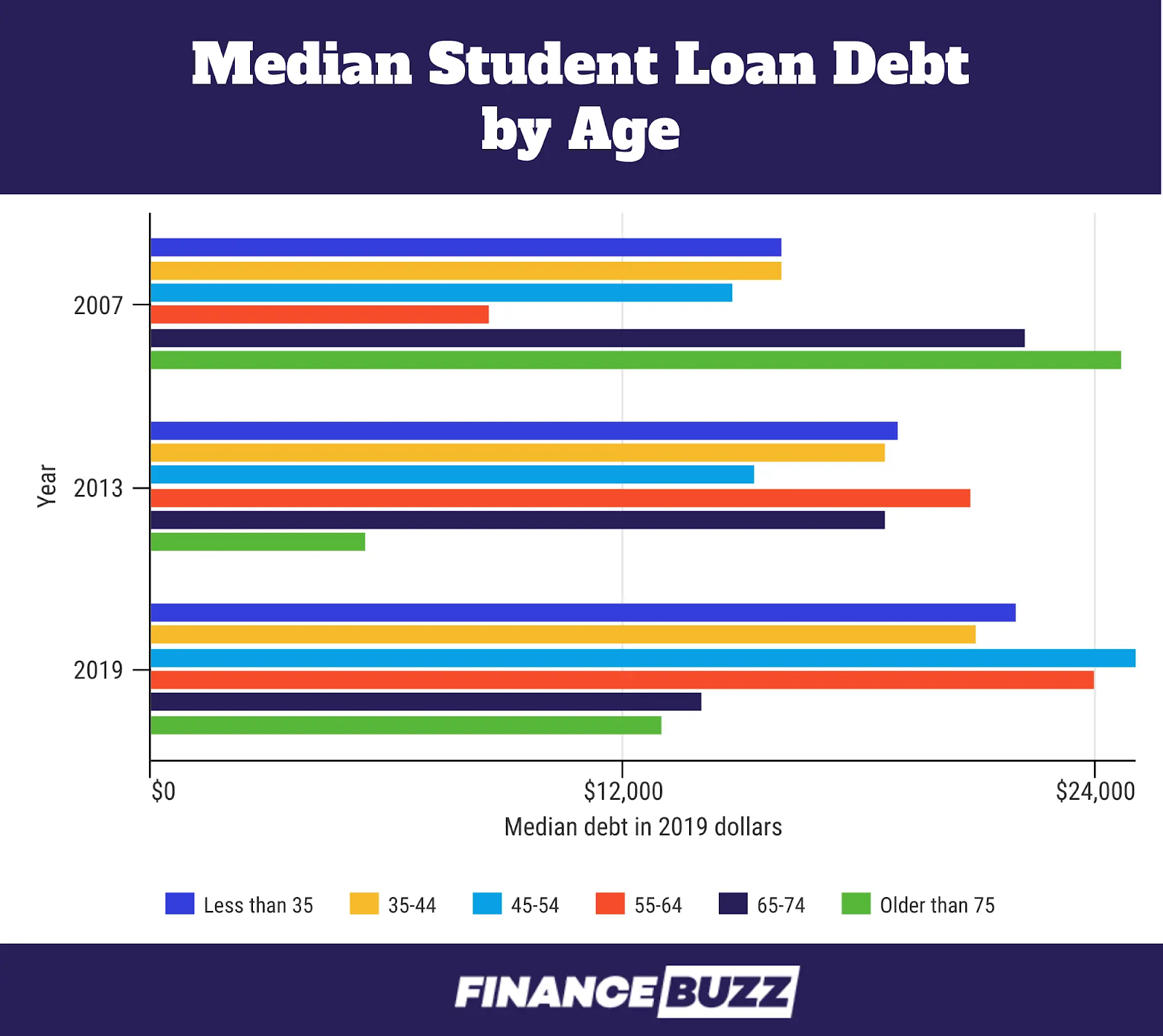

Age plays a significant role in determining someone’s net worth. The older you are, the more earning years you accumulate which is going to have an impact on your net worth. Another huge part of this difference is student loan debt. Remember that your net worth is determined by adding your assets and subtracting your debts. Therefore, higher debt corresponds to a lower net worth. The amount of debt also contributes to home ownership which, as discussed previously, affects your net worth. Student loan debt also negatively impacts one’s investments. A study found that those with persistent student loan debt were less likely to invest in things like stocks, bonds, mutual funds, etc. All of these things impact a person’s earning potential, assets, and net worth.

So What Does This Mean?

There are many things outside of your control that can affect your net worth and your financial stability. You cannot control your family structure, race/ethnicity, age, or marital status. You cannot always control your education level, homeownership status, or region. Your net worth and your worth as a person are not mutually exclusive. Building strong financial habits will help you meet and succeed your goals and get closer to that first million dollars.

Want to learn more about the first three factors that affect financial stability? Click here to check out that article.